Why AIOps Is Key to Cyber Threat Detection in Defense?...

Read More

How AI Transforms Predictive Maintenance in Defense Equipment

How AI Transforms Predictive Maintenance in Defense Equipment In a...

Read More

How to Scale AI Without Breaking Your Infrastructure in 2025

How to Scale AI Without Breaking Your Infrastructure in 2025...

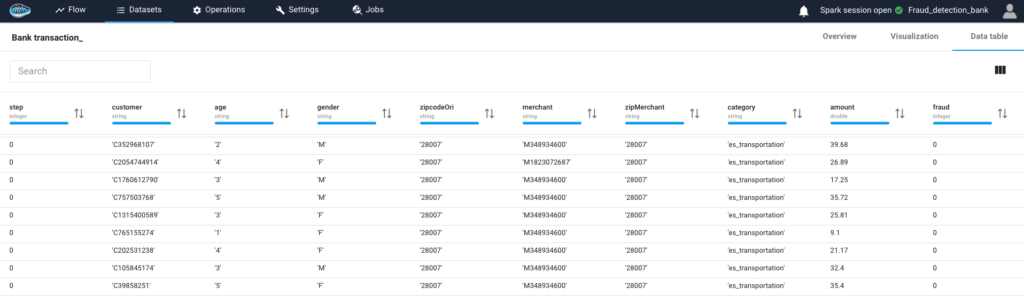

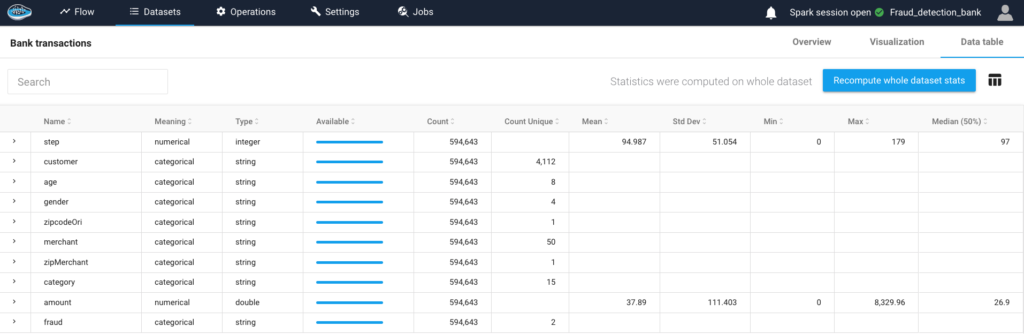

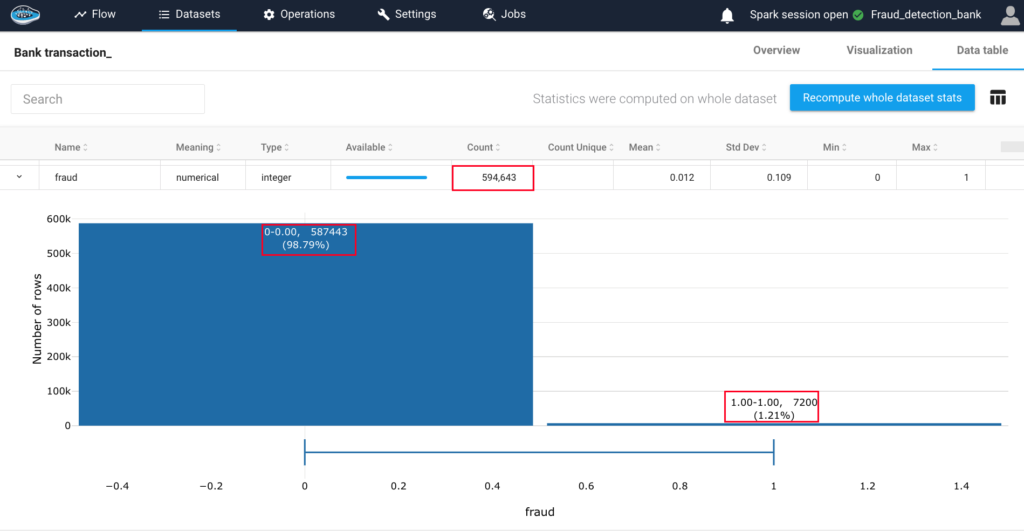

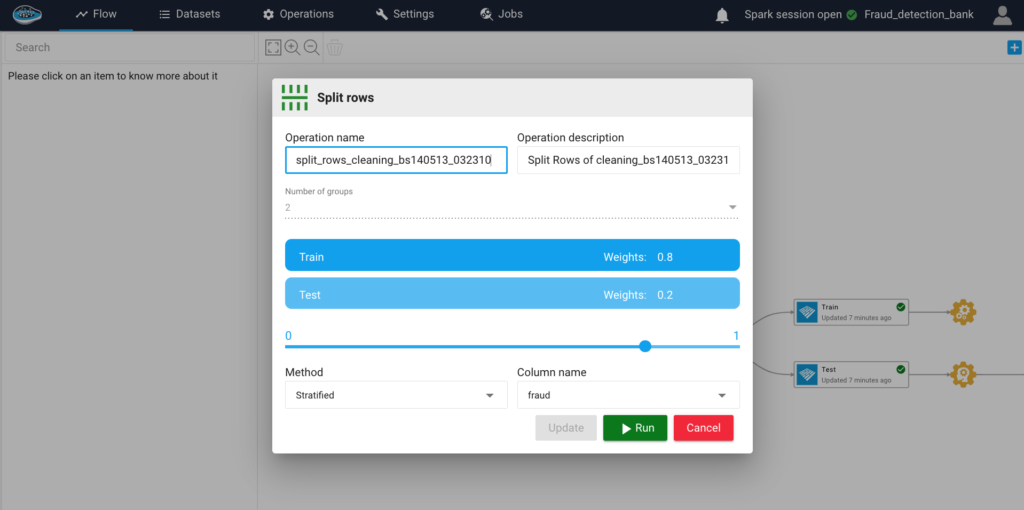

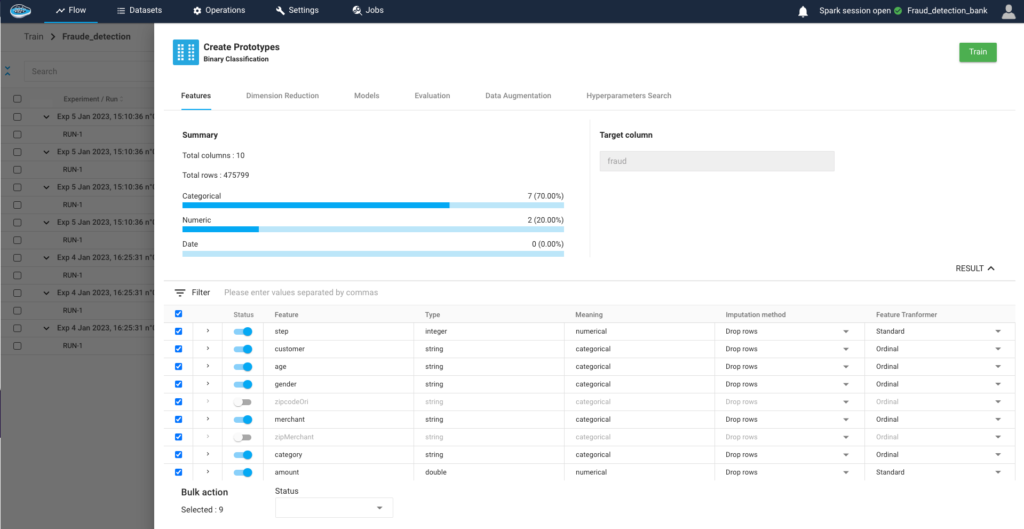

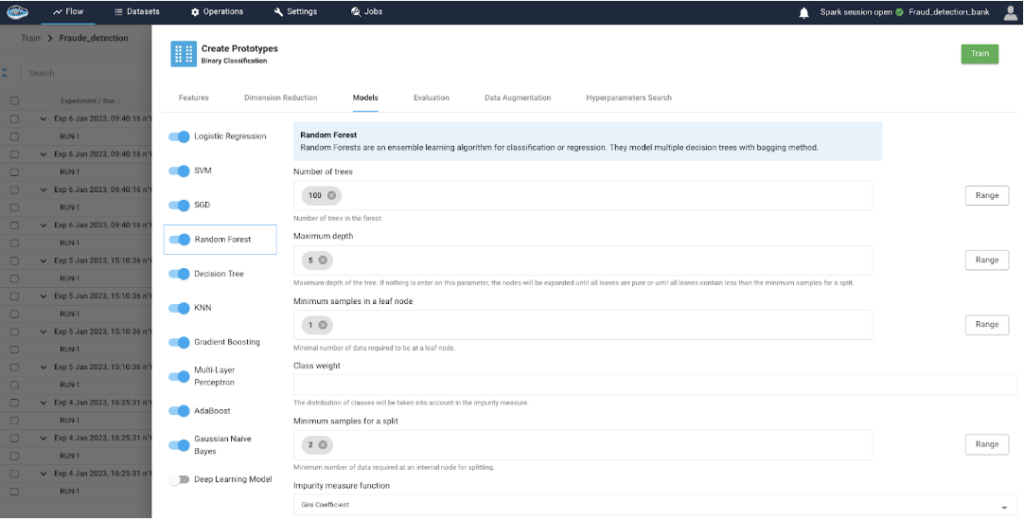

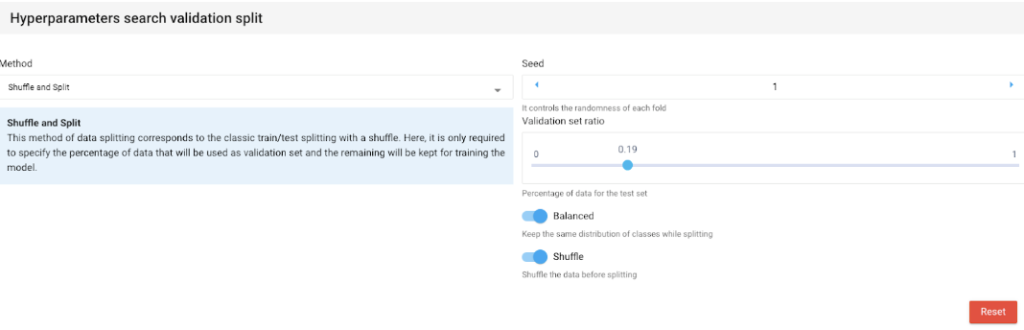

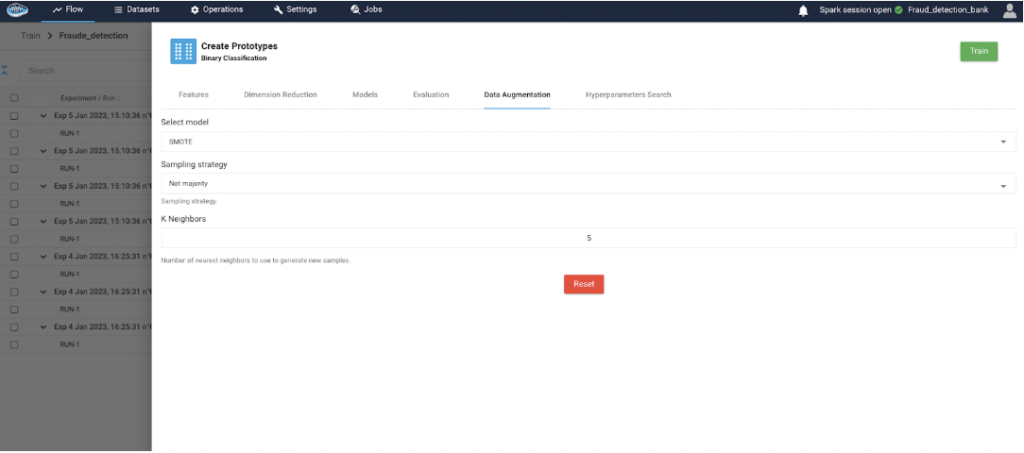

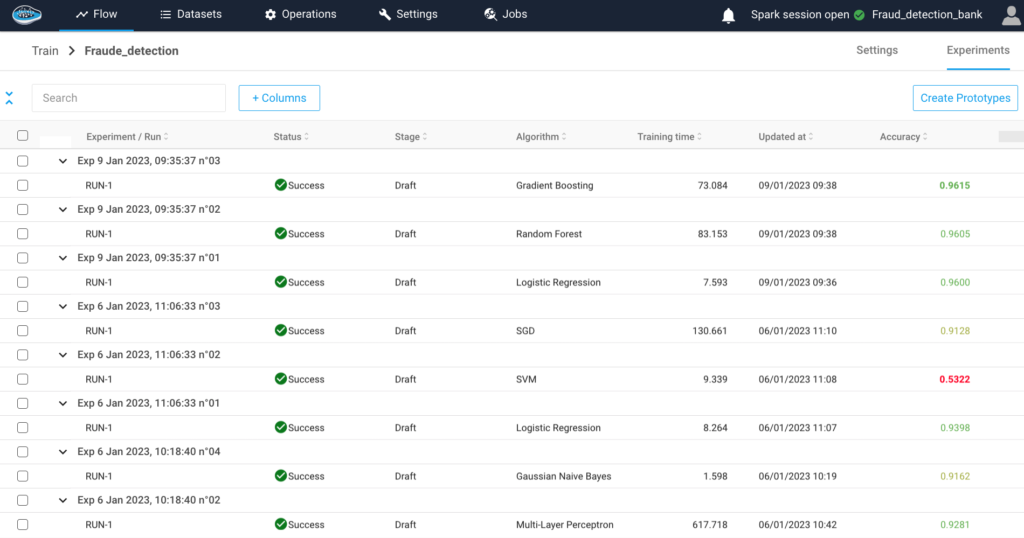

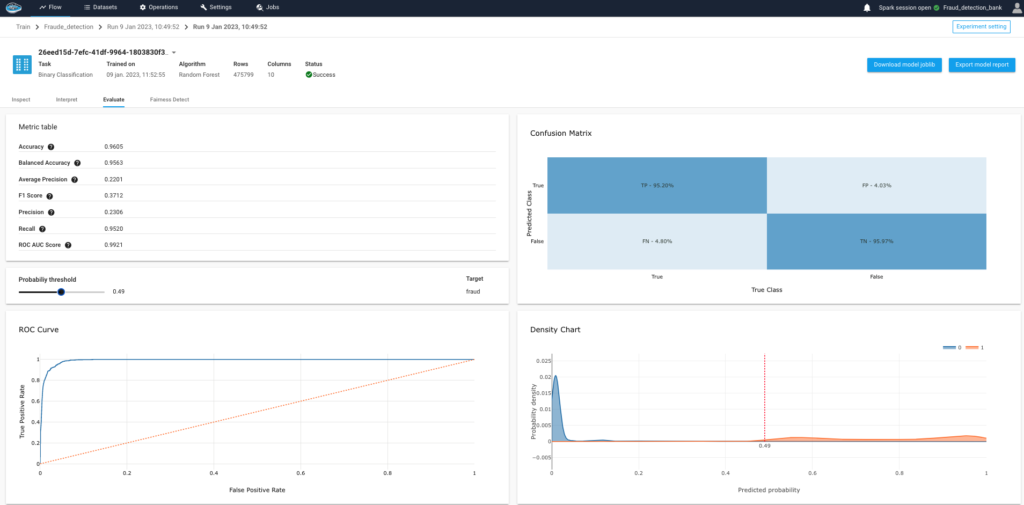

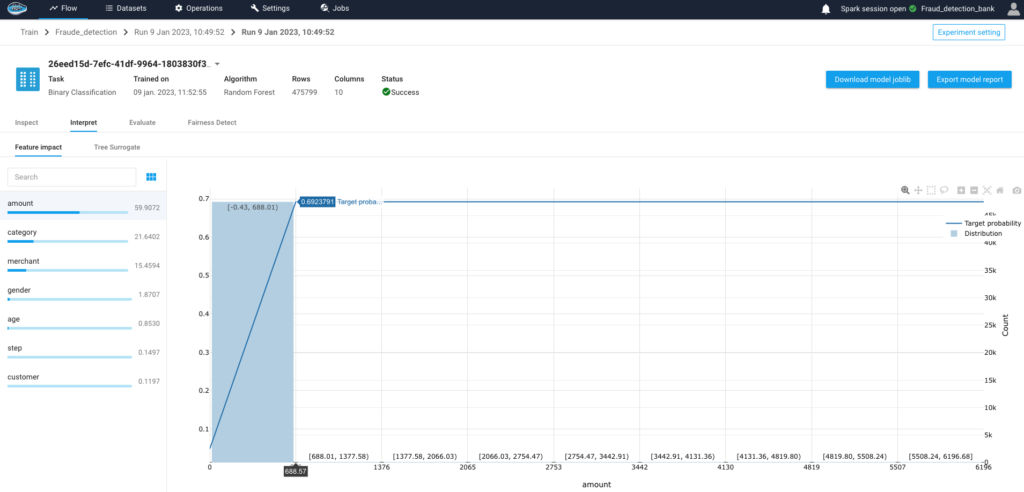

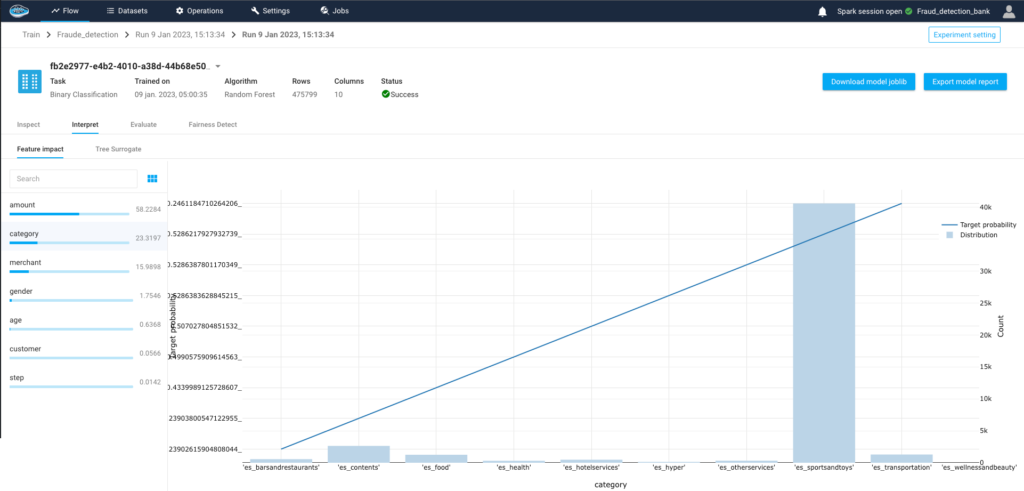

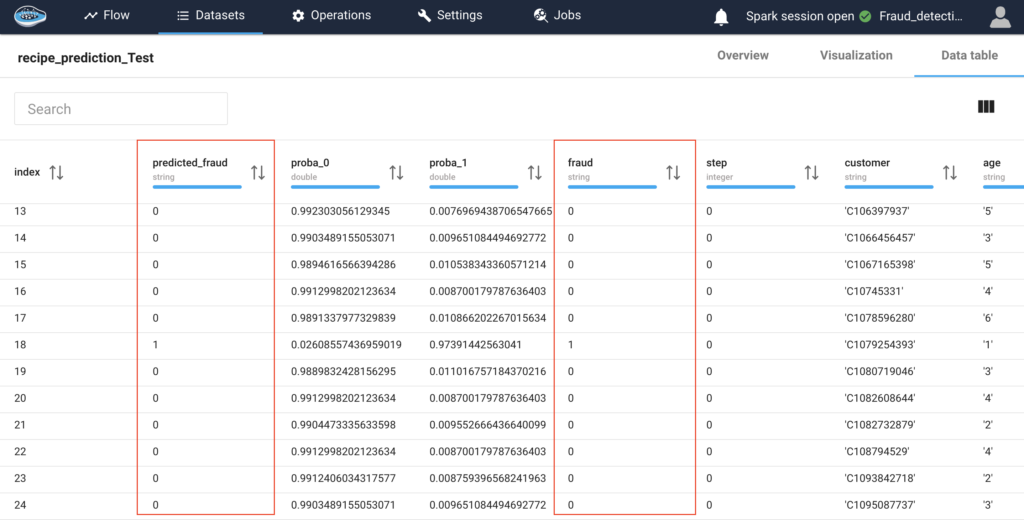

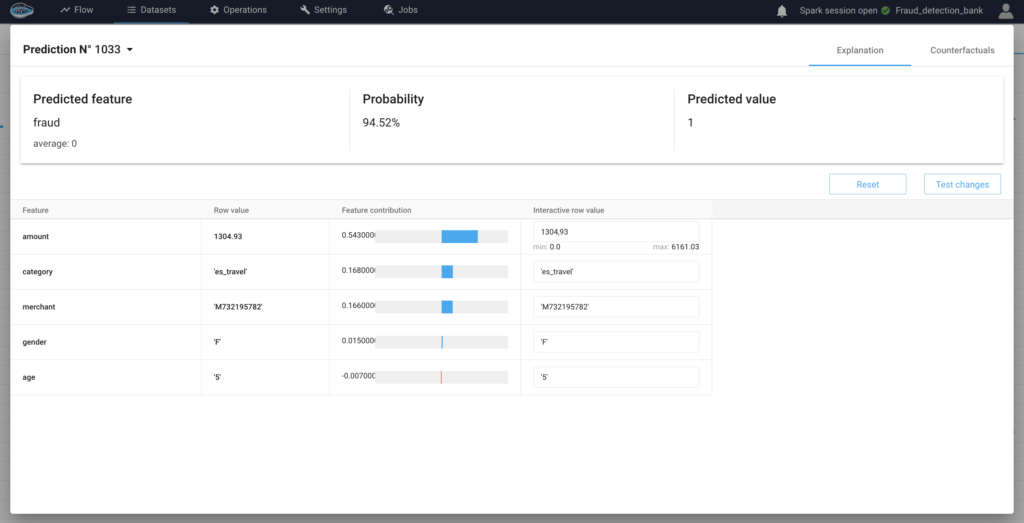

Read MoreHow is papAI transforming fraud detection in Banks ?